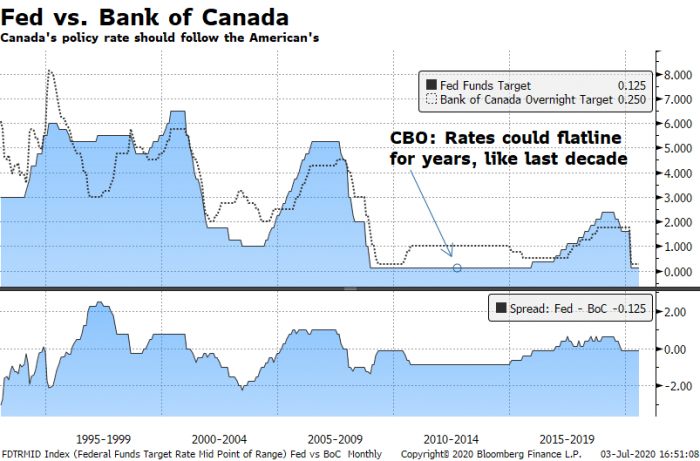

Long Road Back for Jobs: Avid rate watchers all want to know the same thing: how long will unemployment stay elevated? The answer to that is essential to knowing how long rates could remain in a trough. On Thursday, we got a sobering projection from a reputable source. The non-partisan Congressional Budget Office (CBO) says U.S. unemployment will remain “above its pre-pandemic level” into the next decade. Ouch. The CBO forecasts long-term interest rates will climb by the end of 2025, but only by one per cent. If you think about it, that’s almost insignificant historically speaking—and for Canadian rates, the relevance is clear. Ours have a 90%+ correlation with American rates. As for the Fed’s key rate, the CBO predicts it won’t budge until 2026. That’s a long time, but not unprecedented. In the prior cycle rates stayed near zero for six years until December 2015. If the CBO’s forecast proved true, the Bank of Canada would also likely delay or limit rate hikes for 5+ years. Six of the last seven BoC hikes have occurred after the Fed raised first. All this said, forecasts are made to be wrong. That’s why—with the fixed-variable spread being so narrow—risk averse new borrowers can’t be faulted for locking in. (Source: PDF)

BMO cuts: Bank of Montreal has lowered the following special fixed rates:

Matching TD for the lowest openly advertised 5-year fixed from a Big 6 bank.

Stymied Refis: Most 5-year fixed borrowers who got a mortgage just 16 months ago are paying a 120+ basis-point-higher rate than what they’d get today. You can’t blame them for wanting to break their mortgage and reset their rate lower. Getting a better rate is the number one reason people refinance early, according to a rates.ca survey last February. Unfortunately, it’s not as easy as it sounds. Most 5-year fixed borrowers are in high-penalty mortgages that negate most or all rate savings from an early refinance. That said, if you happened to get a 3%+ fixed mortgage from a fair penalty lender a year and a half ago, ask a lender or broker to do the math and see if refinancing makes sense.

S&P Bearish on Canada: “Lingering scars in the form of coronavirus fear, bankruptcies, below break-even oil prices and regulated social distancing will limit…growth for a quarter of the economy in the next year or so,” says the rating agency. “The nature of the shock means there will be permanent losses … It means [Canada’s] economic pie could be 2.5% smaller (in real GDP terms) than pre-pandemic.” S&P also predicts that a “house price correction is in the cards despite lower mortgage rates, and the central bank is expected to remain at an effective lower bound until close to the end of 2022.”

Weaning Off Face-to-Face: “Pre-COVID, Canadians were already shifting to online sources to research mortgage rates and educate themselves,” CanWise founder James Laird told MBN. “However, many still preferred in-person interaction before closing their mortgage. COVID-19 has forced Canadians to complete the process without that in-person appointment. Most have been surprised and impressed with the efficiency and level of service available without requiring an in-person meeting.”

CRA Audits: If you’re a Canadian with U.S. property, read this.

Borrowed 5% Down Payments: CMHC may have ended most forms of borrowed down payments, but that hasn’t stopped some lenders, like Nova Scotia’s Valley Credit Union, from offering them.

Like news like this?

Join our ratespy update list and get the latest news as it happens. Unsubscribe anytime.

Now I am more confused to wait a bit longer for even lower possibly or lock in the 5 year Fixed 2.17 offer.

My online offer is 2.17 called scotia to change the payment amount to what we pay now and she said she can only do 2.2. Even worse making it sound like 1.34 per payment is worth going with her and not worth saving?!?!?! Maybe in 5 years there will not be mortgage specialist at big banks if this is their thinking

Should I stop the gamble and lock in at 2.17 for 5 years

Hi Ashley, Not sure of your circumstances and I didn’t understand this part –> “Even worse making it sound like 1.34 per payment is worth going with her and not worth saving”

But either way, 2.17% is an excellent 5yr fixed rate, assuming a 5yr fixed at a big bank is the right play for you. Just make sure you won’t need to make any major changes to your mortgage for five full years. Major bank IRD penalties can be unpleasant if you’re stung by one.

If you are wanting to pay your mortgage off faster I have a prime rate mtg, simple interest and I can pay amounts to reduce my mtg anytime or even pay it off with no penalty.

log in

log in

5 Comments

Now I am more confused to wait a bit longer for even lower possibly or lock in the 5 year Fixed 2.17 offer.

My online offer is 2.17 called scotia to change the payment amount to what we pay now and she said she can only do 2.2. Even worse making it sound like 1.34 per payment is worth going with her and not worth saving?!?!?! Maybe in 5 years there will not be mortgage specialist at big banks if this is their thinking

Should I stop the gamble and lock in at 2.17 for 5 years

Hi Ashley, Not sure of your circumstances and I didn’t understand this part –> “Even worse making it sound like 1.34 per payment is worth going with her and not worth saving”

But either way, 2.17% is an excellent 5yr fixed rate, assuming a 5yr fixed at a big bank is the right play for you. Just make sure you won’t need to make any major changes to your mortgage for five full years. Major bank IRD penalties can be unpleasant if you’re stung by one.

If you are wanting to pay your mortgage off faster I have a prime rate mtg, simple interest and I can pay amounts to reduce my mtg anytime or even pay it off with no penalty.

Seems like variable rate is the best way to go forward. Right?

Mos, Depends. See: https://www.ratespy.com/fixed-or-variable-rate-the-decision-checklist-02223752