log in

log in

—The Mortgage Report: Oct. 13—

- If you like definitive-sounding rate calls, here’s one: “The 2020 recession AND the 40-year bond rally are over,” declares Bank of America.

- Positive economic data surprises, declining uncertainty post-U.S. election and “massive monetary and fiscal policy support” will “set the stage” for higher bond yields, the bank stated in a report on Tuesday. If true, it would mean higher fixed mortgage costs—in Canada too, given our linkage with U.S. rates.

- By year-end, BofA is looking for a quarter-point bounce in one of the world’s most-watched rates, the 10-year Treasury. (The 10-year has a solid correlation with fixed mortgage rates north and south of the border.) But there’s a risk that investors “rush to the exits on bonds” and cause a “disorderly overshoot to the upside” (in rates), it adds. BofA says the 10-year yield could pop 0.75 to 1.25 percentage points higher by the end of next year. Economists overall are currently forecasting a 0.85 percentage point increase in that timeframe.

- On this side of the border, economists don’t see rates rising nearly as much. If Canadian forecasters are right (and everyone knows how often they’re not), Canada’s 5-year yield will climb just 0.45 percentage points by year-end 2021. The Bank of Canada will do its part to limit that increase by continuing to purchase bonds, thus weighing down fixed mortgage rates for the foreseeable future.

- If BofA’s call is even partially right, however, it supports our view that the risk/reward of variable rates just isn’t there anymore for most borrowers. That’s assuming one chooses a fixed rate from a fair-penalty lender. Floating rates are simply less appealing when:

- 5-year fixed mortgages are selling for the same price as variables

- rates are so close to 0% already

- the economy is near the bottom of a business cycle

- the BoC is messaging that it’s likely finished cutting rates.

- All this said, forecasts are often barely worth the paper (or web page) they’re written on. No one knows how this pandemic will play out. While we all wait to see how this story ends, one thing’s for certain. Until Canada’s 5-year bond yield closes above 0.55%, there’s little risk of a material boost to fixed rates.

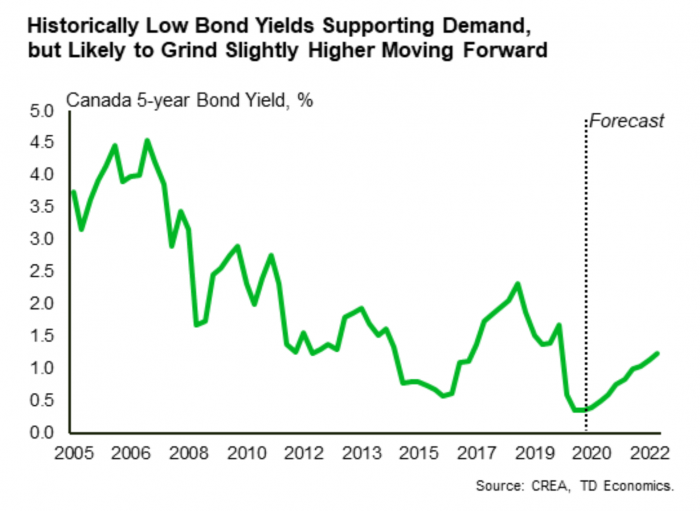

Below 1% and Holding

- “The Canadian 5-year bond yield is currently near historic lows and is likely to stay sub 1% through next year,” says TD Economics.

- “…We expect some modest upward drift in bond yields from their current rock-bottom levels,” it adds, “reflecting continued economic recovery.”

- Sub-1% sounds pretty low, and it is. But TD’s forecast implies 5-year fixed rates could jump up to 6/10ths of a percentage point from here. That would result in roughly $3,000 more interest per $100,000 of mortgage on a 5-year fixed…if it happens.

Quick Hits…

- Canadians have come to know Canada’s largest private default insurer as “Genworth” for a quarter century. Now it’s called Sagen.

- 76% of the three million Canadian jobs lost in March/April have been recovered. But construction jobs are still down 120,000 versus pre-pandemic. (Home Builder Magazine)

- The temporary nature of government income assistance “overstates housing fundamentals,” CMHC’s chief economist said recently on a conference call.

10 Comments

Do you guys think there is still time to take a 1 year fixed and lock into a 5 year fixed next year?

Hi Kim, Maybe but like Northwin says, it’s a gamble. Statistically there’s a meaningful chance that the 5yr government yield (and hence 5yr fixed rates) will be higher in one year. We’ll run numbers on this in tonight’s story.

President Trump is doing whatever he can to get reelected!

Not sure anyone knows the answer to this but how far in advance of BOC increases do bond yields usually start increasing?

HI Mrtgman, Government bond yields usually jump at least 2-6 months before the Bank of Canada hikes its policy rate. Sometimes less if it’s a surprise due to an economic shock, and sometimes more if it’s well telegraphed by the Bank.

Kim: That sounds like a pure gamble. No one knows the future. What if 5-yr fixed rates go up .5% between now and then. How are you ahead?

I have 3 years left on a variable rate. I am undecided in whether I should lock in now or let it run it’s course for the balance of the term. Do you have any thoughts on this.

Hi Barry, There are lots of necessary questions before an answer can be given, like:

What is your discount from prime?

Who is the lender?

Is it a low-frills mortgage with restrictions?

What is your financial situation (fallback assets, home equity, employment status, monthly debt load, etc.)?

What are your 5yr goals (will you move, sell and rent, need more money, etc.)?

Well the BoC announced that it will stop buying Mortgage Bonds, that will most likely cause the interest rates to rise again.

Hi Garry, Lenders have a lot of different funding sources of which CMBs are just one. But yes, we’d expect a slight bullish response in mortgage rates, other things equal.